Mortgage Rates Update—Additional

This newsletter is short, simpler to understand and I am including lots of pictures.

When it comes to mortgage rates, the news are about a week behind.

I am able to supply up to the minute information because we pay a monthly subscription to a professional service and in this manner we are able to see the hour by hour changes in mortgage rates.

This is useful when we lock rates for our clients' loans. We time them so they get the best possible deal - that's the main reason we pay for this service.

Between January 05 and February 23 there was a window of opportunity to get low mortgage rates. The 30 years rate dropped as low as 5.25% and I have not seen this since 2022.

Quick Reminder: these graphs represent pricing for Mortgage Bonds. When bonds go up, rates go down. When bonds go down, rates go up. Bond pricing has an inverse relationship to Mortgage Rates.

As of March 2nd the tide has turned and rates have resumed their up trend, as you can see below.

Some clients say to me "but Alejandro when are the rates finally going to come down!" I have another client who says to me "the Government will have to do something, they cannot allow rates to go higher".

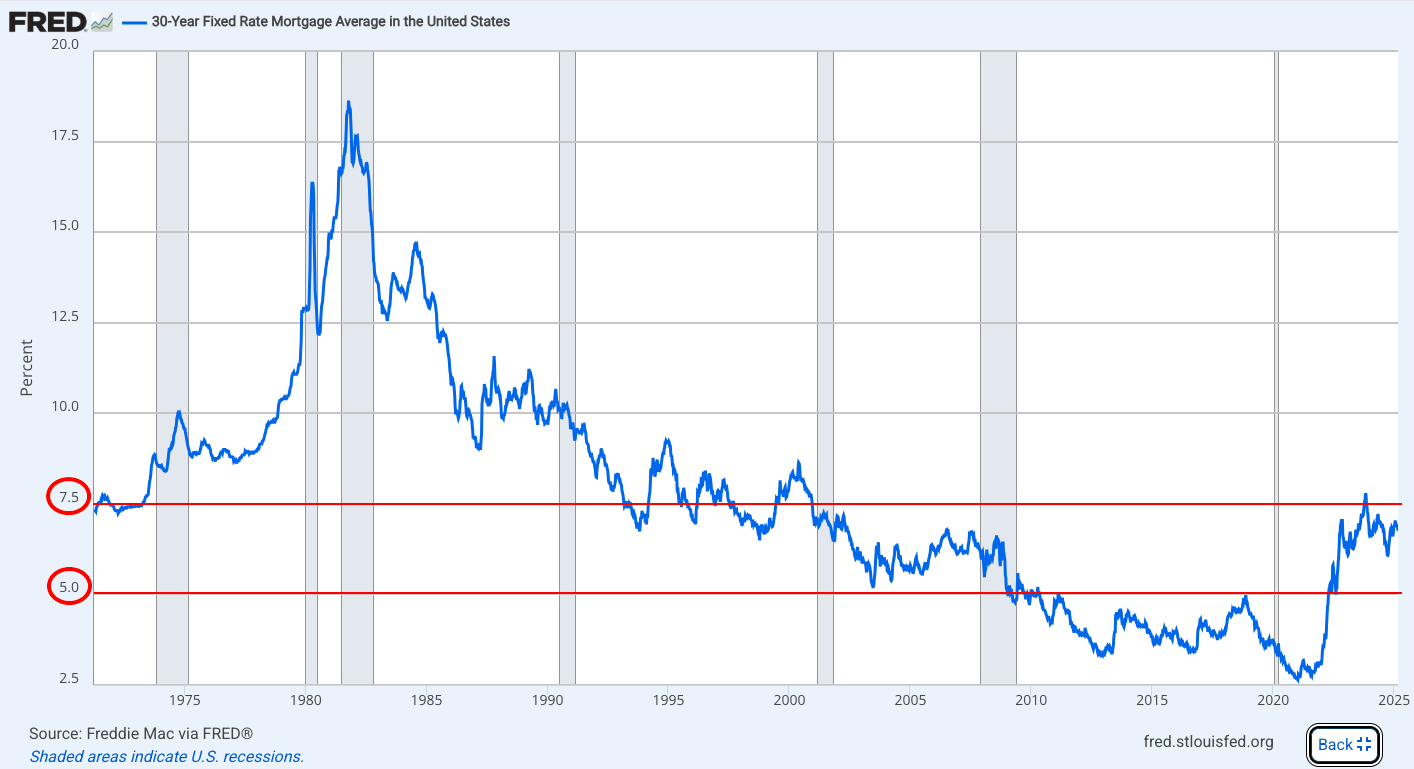

For 40 years, since 1981 until end of 2021, rates consistently went lower and lower.

Unless you are older, (like me) most people have never seen anything other than low rates.

This is what rates did for 40 years:

I would also like to give you another perspective.

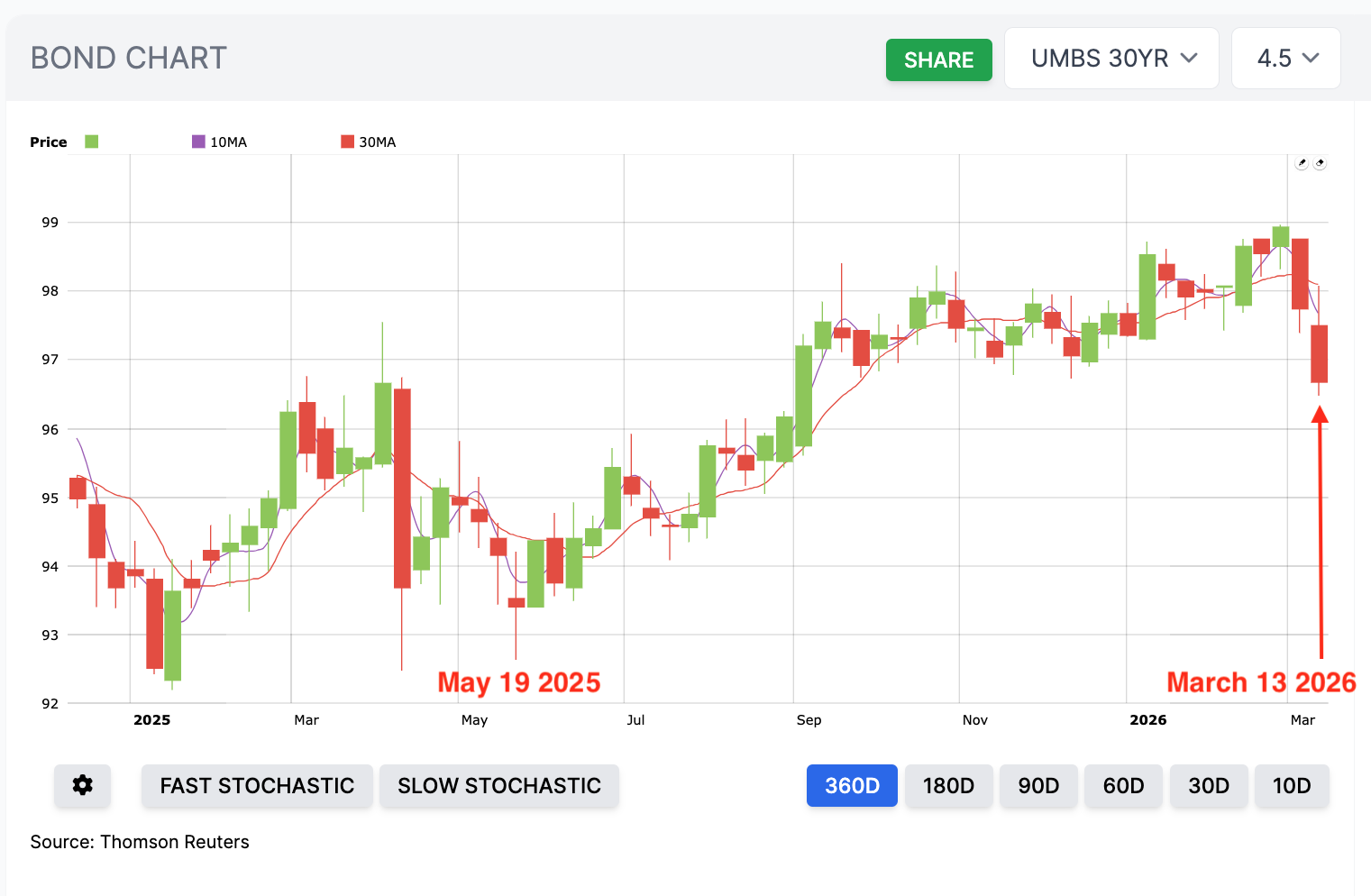

In terms of Rates this is where we are now compared to 1 year ago:

As you can see rates in March 13 2026 are still much better than what they were in May 19 2025.

In other words, if you were looking for the super low window of opportunity to refinance - that window is gone for now, but we are still in a relatively low rate environment.

Will it come back, yes, later on this year.

How long would it last? I have seen sharp drops stay low from anywhere between 3 days to 1 month.

It is almost impossible to predict how long the low would last.

If this is what you are after, being prepared is key. Most lenders want the loan in their system and sometimes already approved by an underwriter before they would allow you to lock the rate.

Advanced preparation is KEY.

Should you or anyone else be held hostage to the rate? In other words, do you need to put your life on hold pending what happens with the rate?

I would like to leave you with a thought:

My most successful clients, even though they are mindful of the rate and its direction, and do try to get the best deal they can, the rate is not the determining factor which propels their decisions.

They usually have a business plan, a strategy, which is rate independent. They use the money to achieve a particular goal which, to them, is worth many times over whatever rate is being offered by the market at any particular time.

The loan is just a vehicle to achieve their dreams. They put all their energy on the dream/project.

If you are contemplating such a dream or project, don't hesitate to do a brainstorming consultation with me. Half of my time is spent listening to my clients' projects and advising them.

Over the years I have accumulated a wealth of information from my successful clients which I make available to all my clients!

I hope this information added some value to you.